Assessing the Likely Effectiveness of the Federal Reserve’s September Rate Cut

To assess whether the Federal Reserve’s September rate cut is likely to be effective, it is important to move beyond the assumption that lower interest rates automatically stimulate spending. Instead, the effectiveness of the cut depends on expectations, confidence, and the underlying causes of rising unemployment.

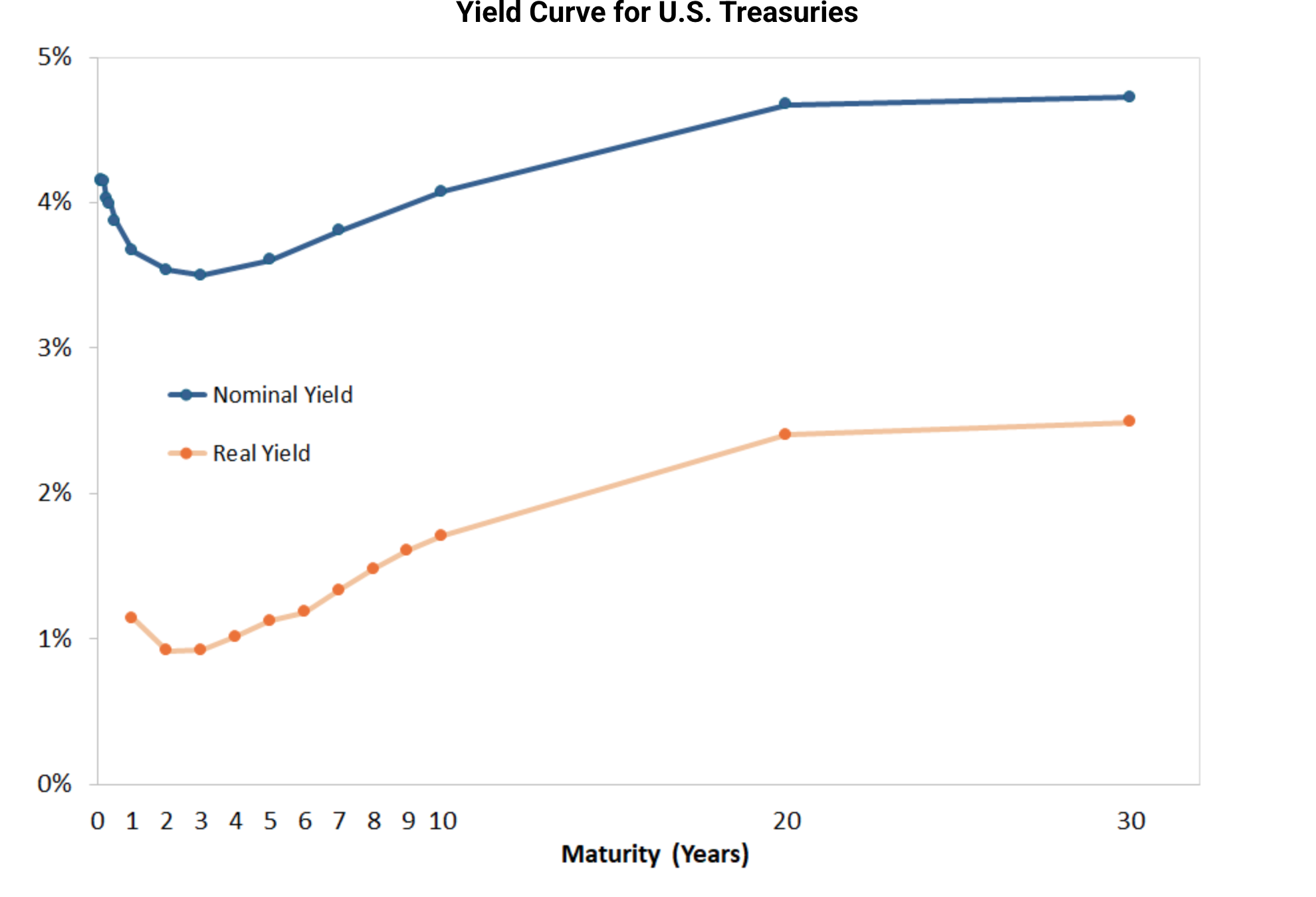

Yield Curve

At the time of the September cut, the yield curve was notably steep in the medium term. Short-term yields were elevated, while yields around the 2–3 year horizon were significantly lower, before rising again at longer maturities. This structure indicated that markets had already priced in substantial future rate cuts.

In other words, the September cut did not represent a surprise. Borrowers and investors had long expected interest rates to fall further over the coming years. As a result, the immediate incentive to borrow following the cut was limited. If economic agents believe that rates will continue to decline, many will rationally delay borrowing until they expect rates to reach their lowest point.

This weakens the traditional transmission mechanism of monetary policy: rather than accelerating borrowing and spending, the cut largely confirmed an existing trend that had already been incorporated into expectations.

Consumer Confidence

Consumer confidence provides further insight into why the rate cut may have had limited immediate impact on aggregate demand. Confidence fell sharply earlier in the year, declining from 71 in January to a low of 52 in May. Although it recovered slightly in the months leading up to September, reaching 58.2 in August, it remained deeply depressed, falling again to 55.1 in September.

Such persistently low confidence suggests that households were increasingly uncertain about future economic conditions. News surrounding layoffs, immigration policy, and broader political and economic instability weighed heavily on sentiment. This uncertainty was already beginning to affect consumer behaviour, particularly as unemployment began to rise again.

In this context, the September rate cut was unlikely to trigger a significant increase in discretionary spending. However, it may have played a different, subtler role: restoring some degree of predictability. By acting, the Fed signalled that it was attentive to deteriorating conditions and willing to respond. While this may not immediately boost consumption, it helps prevent confidence from deteriorating further — a crucial function during periods of heightened uncertainty.

Labour Market Dynamics

Perhaps the most important factor in evaluating the effectiveness of the rate cut lies in the nature of rising unemployment itself. Layoffs have been concentrated in the technology sector and in government employment. These are not sectors that respond strongly to marginal changes in interest rates.

Tech layoffs largely reflect structural adjustments, cost discipline, and post-boom correction rather than a sudden collapse in consumer demand. Government job reductions, meanwhile, are driven by fiscal and political decisions, not monetary conditions.

This interpretation is reinforced by labour market indicators. The Beveridge Curve shows that the job openings-to-unemployment ratio fell to 0.97 in August and recovered slightly to 1.007 in September. This indicates a cooling labour market, but not a collapse in labour demand. Firms are becoming more cautious, not desperate.

This suggests that unemployment is rising primarily due to higher costs, uncertainty, and structural adjustments rather than insufficient consumer spending. In such an environment, interest rate cuts are inherently less effective at stimulating hiring.

Overall Assessment

Taken together, these factors suggest that the Federal Reserve’s September rate cut was unlikely to generate a strong, immediate increase in borrowing, spending, or employment. Expectations of further cuts, weak consumer confidence, and cost-driven unemployment significantly reduced the policy’s stimulative power.

However, this does not imply that the cut was meaningless. Rather than acting as a growth accelerator, the rate cut functioned as a stabilising measure. It helped anchor expectations, reduce uncertainty, and prevent a sharper deterioration in confidence and hiring intentions. In this sense, the policy was defensive rather than expansionary.

Ultimately, the effectiveness of the September rate cut should not be judged by whether it triggered a surge in spending, but by whether it prevented existing weaknesses from escalating into a broader economic contraction.